StudentShare

Our website is a unique platform where students can share their papers in a matter of giving an example of the work to be done. If you find papers

matching your topic, you may use them only as an example of work. This is 100% legal. You may not submit downloaded papers as your own, that is cheating. Also you

should remember, that this work was alredy submitted once by a student who originally wrote it.

✕

Free

Efficient Market Hypothesis - Essay Example

Summary

The paper "Efficient Market Hypothesis" is a perfect example of a finance and accounting case study. Strong Form Efficient Markets – This form of the efficient market holds that the investors are aware of every kind of information about the market which includes all past information, publicly available information and private information…

- Subject: Finance & Accounting

- Type: Essay

- Level: Undergraduate

- Pages: 5 (1250 words)

- Downloads: 0

- Author: afay

Extract of sample "Efficient Market Hypothesis"

a) Efficient Market Hypothesis s that stock prices reflect the information of the market. It has three forms: Strong Form Efficient Markets – This form of efficient market holds that the investors are aware of every kind of information about the market which includes all past information, publicly available information and the private information.

Semi-Strong Form Efficient Markets - This form of efficient market holds that the investors are aware of relatively less amount of information about the market which includes all past information and publicly available information.

Weak Form Efficient Markets – This form of efficient market holds that the investors are aware of very less amount of information about the market which includes only the past information.

c)

The Relationship between the number of assets in a portfolio and the risk of the portfolio is negative or inverse such that if number of assets increases, the overall risk of the portfolio will reduce.

Portfolio Risk

Number of Assets in a portfolio

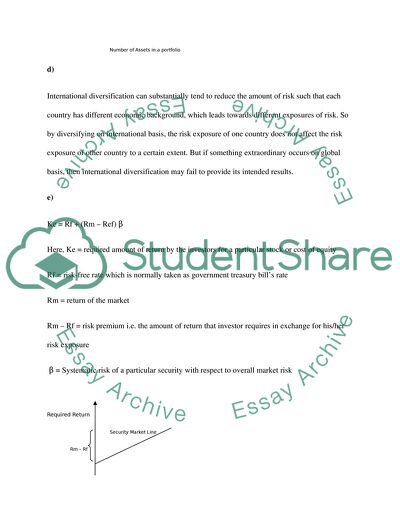

d)

International diversification can substantially tend to reduce the amount of risk such that each country has different economic background, which leads towards different exposures of risk. So by diversifying on international basis, the risk exposure of one country does not affect the risk exposure of other country to a certain extent. But if something extraordinary occurs on global basis, then international diversification may fail to provide its intended results.

e)

Ke = Rf + (Rm – Ref) β

Here, Ke = required amount of return by the investors for a particular stock or cost of equity

Rf = risk-free rate which is normally taken as government treasury bill’s rate

Rm = return of the market

Rm – Rf = risk premium i.e. the amount of return that investor requires in exchange for his/her risk exposure

β = Systematic risk of a particular security with respect to overall market risk

Required Return

Security Market Line

Rm – Rf

Rf

Risk

f)

Security Market Line depicts the position of a company in terms of return at a given level of risk. If the investors become less averse which means that they are ready to take more risk, then, they will chose a company which is positioned at a higher point on the “SML” therefore, the shareholders will demand a higher rate of return.

g)

Capital Structure can be defined as the financing mix of a firm such that it describes the percentage of equity and debt involved in the financing mix of the firm. For instance, if a firm has included 60% equity in its total financing and 40% debt then the capital structure would be called as 60:40.

i)

The two ways in which shareholders can demand a return from the company are capital gains and the dividends. Generally the marginal tax rate on dividends is higher than that of capital gains. Therefore, the investors prefer to the capital gains as they are not taxed unless they are realized.

j)

Among residual dividend policy and constant payout ratio dividend policy, the policy that delivers stable cash payment of dividend is constant payout ratio dividend policy. The reason for choosing this policy is that whatever the amount of income is earned, a specific percentage of that income must be distributed to the shareholders. However, for residual dividend policy, the firm retains the amount of profit for the upcoming future opportunities. If any amount is left after fulfilling this purpose, then it is distributed to the shareholders. Therefore constant payout ratio effectively ensures stable cash payments of dividends.

References

Baker, H. Kent . and Martin, Gerald S., 2011.Capital Structure and Corporate Financing Decisions: Theory, Evidence, and Practice. New York: John Wiley & Sons.

Berk, Jonathan B. and DeMarzo. Peter M., 2010. Corporate finance. 2nd ed. New York: Prentice Hall.

Bierman, Harold., 2003. The capital structure decision. New York: Springer.

Brigham, Eugene F. and Ehrhardt, Michael C., 2008. Financial management: theory and practice. 12th ed. New York: Cengage Learning.

Eckbo, Bjørn Espen., 2008. Handbook of corporate finance: empirical corporate finance. Oxford: Elsevier.

Jaffe, Jeffrey. and Ross, Randolph Westerfield., 2004. Corporate Finance. New Delhi: Tata McGraw-Hill Education.

Khan, M. Y., 2004. Financial Management: Text, Problems And Cases. 2nd ed. New Delhi: Tata McGraw-Hill Education.

Shim, Jae K. and Siegel, Joel G., 2008. Financial Management. 3rd ed. Oxford: Barrons Educational Series.

Vishwanath, S. R., 2007. Corporate Finance: Theory and Practice. 2nd ed. California: SAGE.

Watson, Denzil. and Head, Antony., 2009, Corporate Finance Book and MyFinancelab Xl. 5th ed. New York: Pearson Education, Limited.

Read

More

sponsored ads

Save Your Time for More Important Things

Let us write or edit the essay on your topic

"Efficient Market Hypothesis"

with a personal 20% discount.

GRAB THE BEST PAPER